Medicare 101

How to Choose the Best Medigap Plans: Simple Guide for Seniors (2024)

Did you know that approximately 25% of Medicare beneficiaries—around 15 million people—purchase Medigap plans to help cover their healthcare costs?

Understanding Medigap and How It Works

Medicare Supplement Insurance, commonly known as Medigap, serves as a vital financial safety net for millions of Americans enrolled in Original Medicare. Over 14 million Americans had Medicare Supplement insurance in 2018, highlighting its importance in the healthcare landscape. This section explains what Medigap is, how it differs from other options, and what it covers.

What is Medigap insurance?

Medigap is supplemental insurance sold by private companies designed specifically to fill the "gaps" in Original Medicare coverage. These policies work alongside Medicare Parts A and B to cover out-of-pocket expenses that would otherwise come directly from your wallet.

To purchase a Medigap policy, you must be enrolled in both Medicare Part A (Hospital Insurance) and Part B (Medical Insurance). Once you have a policy, Medicare pays its share of approved healthcare costs first, then your Medigap policy kicks in to pay its portion.

What makes Medigap distinct is that these policies are standardized by federal and state regulations. In most states, there are 10 different standardized plans labeled with letters (A through N), each offering a specific set of benefits. No matter which insurance company sells a particular letter plan, the basic benefits remain identical—only the premiums differ.

How Medigap differs from Medicare Advantage

Although both options provide additional coverage beyond Original Medicare, Medigap and Medicare Advantage are fundamentally different approaches:

- Different purpose: Medigap supplements Original Medicare, whereas Medicare Advantage (Part C) is an alternative way to get your Medicare benefits.

- Coverage approach: With Medigap, you maintain your Original Medicare coverage and add supplemental insurance. Medicare Advantage replaces Original Medicare with a bundled plan from a private insurer.

- Provider access: Medigap allows you to see any doctor who accepts Medicare nationwide. Medicare Advantage typically restricts you to a network of providers.

- Coordination: You cannot use Medigap while enrolled in a Medicare Advantage plan.

- Drug coverage: Medigap plans sold after 2005 don't include prescription drug coverage, requiring a separate Part D plan if needed.

What Medigap policies cover and don't cover

Medigap helps with expenses that Original Medicare doesn't fully cover. All standardized Medigap policies include these core benefits:

- Part A coinsurance and hospital costs up to an additional 365 days after Medicare benefits are used up

- Part B coinsurance or copayment

- First three pints of blood

- Part A hospice care coinsurance or copayment

Depending on the specific plan, additional coverage may include:

- Skilled nursing facility care coinsurance

- Medicare Part A deductible ($1676 in 2025)

- Medicare Part B deductible (only for plans C and F for those eligible before January 1, 2020)

- Part B excess charges

- Foreign travel emergency care

Nevertheless, Medigap has clear limitations. These policies generally don't cover:

- Long-term care (nursing home care)

- Vision or dental care

- Hearing aids

- Eyeglasses

- Private-duty nursing

Furthermore, Medigap policies only cover one person. If both you and your spouse want coverage, you'll each need to purchase separate policies.

The standardization of Medigap makes comparison shopping easier, though premiums can vary substantially between insurers. Some plans may cost as little as $30-$40 monthly while others exceed $400 per month, making it essential to compare options carefully.

Types of Medigap Plans Available in 2024

In 2024, Medicare beneficiaries can choose from several standardized Medigap plans, each identified by a letter and offering specific benefits. Understanding these options helps you select coverage that best addresses your healthcare needs and budget.

Overview of Medigap plans A through N

Currently, insurance companies offer up to 10 standardized plans labeled A, B, C, D, F, G, K, L, M, and N. The standardization ensures that plans with the same letter provide identical basic benefits regardless of which company sells them or where you live.

Plan G has become the most popular option, accounting for 39% of all Medigap policyholders (approximately 5.3 million people) in 2023. Plan F follows closely at 36% (nearly 4.9 million people), with Plan N in third place at 10% (about 1.4 million people).

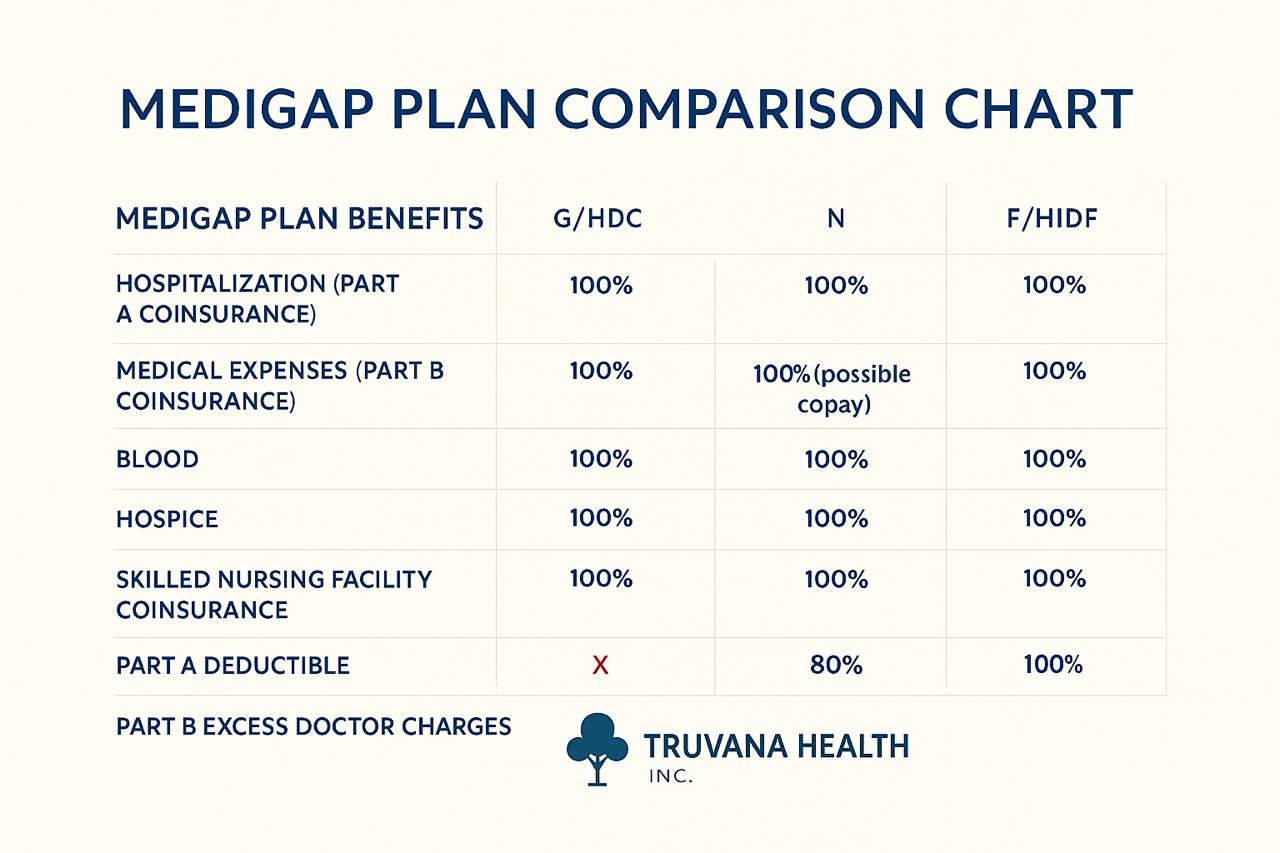

All Medigap plans cover certain core benefits, including Part A coinsurance and hospital costs for up to 365 additional days after Medicare benefits are used up. Additionally, most plans cover the Part B coinsurance or copayment fully, except Plans K and L which cover 50% and 75% respectively.

The more comprehensive plans also cover:

- Skilled nursing facility care coinsurance

- Part A deductible

- Foreign travel emergency care (up to plan limits)

- Part B excess charges (only Plans F and G)

Plans no longer available to new enrollees

Since January 1, 2020, Medigap plans C and F are no longer available to people newly eligible for Medicare. This change resulted from federal legislation prohibiting new Medigap plans from covering the Medicare Part B deductible. People who were Medicare-eligible before January 2020 can still purchase these plans. Likewise, those already enrolled in Plans C or F can keep their coverage.

Prior to June 2010, additional plans including E, H, I, and J were available. Plan J was particularly notable as it included prescription drug coverage and benefits for at-home recovery and preventive services. These benefits became obsolete with the creation of Medicare Part D and expanded Original Medicare coverage.

High-deductible and cost-sharing options

For those seeking lower monthly premiums, several alternative options exist:

- High-Deductible Plans: Some states offer high-deductible versions of Plans F and G. With these options, you must pay out-of-pocket expenses up to the deductible amount—$2,800 in 2024 and $2,870 in 2025—before the policy begins paying benefits.

- The high-deductible version of Plan F is only available to beneficiaries eligible for Medicare before January 1, 2020, while high-deductible Plan G is available to those eligible on or after that date.

- Cost-Sharing Plans: Plans K and L offer partial coverage for certain benefits:

- Plan K covers 50% of several benefits including Part B coinsurance and the Part A deductible, with an annual out-of-pocket limit of $7,220 in 2025.

- Plan L provides 75% coverage for these same benefits with a lower out-of-pocket limit of $3,610 in 2025.

- Once you reach these limits, the plans pay 100% of covered services for the remainder of the year.

Note that Minnesota, Massachusetts, and Wisconsin standardize their Medigap policies differently from other states, offering their own unique plan structures.

How to Compare Medigap Plans Effectively

Comparing different Medigap plans might seem overwhelming at first, yet the standardized nature of these policies makes the process more straightforward than you might expect. Consequently, with the right approach, you can find coverage that fits both your healthcare needs and budget without unnecessary confusion.

Using a Medigap comparison chart

The Medigap comparison chart is your essential starting point for evaluating plan options. Medicare publishes an updated chart annually that displays all standardized plans side-by-side. This visual tool allows you to quickly see which benefits each plan includes and at what percentage they're covered.

To access this helpful resource, visit Medicare.gov/medigap-supplemental-insurance-plans and enter your ZIP code. This search provides plans available in your area along with their specific details. The chart uses checkmarks to indicate 100% coverage of benefits, while percentage signs show partial coverage.

Comparing benefits side by side

When analyzing different plans, focus primarily on these key factors:

- Coverage needs: Assess which healthcare services you use most frequently

- Monthly premiums: Compare costs across companies for the same lettered plans

- Out-of-pocket costs: Consider deductibles, copayments, and coinsurance

- Annual limits: Note the out-of-pocket maximums for Plans K ($7,220 in 2025) and L ($3,610 in 2025)

Remember to evaluate the complete financial picture. For instance, add up the monthly premium, annual Part B deductible, and any applicable copayments to determine the true cost. Initially, higher premium plans often provide better value for those with frequent healthcare needs.

Understanding plan standardization

Perhaps the most critical concept when comparing Medigap policies is standardization. Insurance companies must follow federal and state laws when selling these policies, making them "standardized".

The benefits in each lettered plan remain identical regardless of which insurance company sells it. For example, Plan G from one company offers exactly the same benefits as Plan G from another. The only difference between policies with the same letter is the premium amount.

This standardization means you should never compare different lettered plans (like Plan G versus Plan N) without understanding their distinct benefit structures. Instead, compare the same plan letter across different insurers. Premium differences for identical coverage can be substantial—sometimes hundreds of dollars annually—making comparison shopping exceptionally valuable.

When and How to Enroll in a Medigap Plan

Timing proves critical when enrolling in Medigap plans, as your decision window significantly impacts both coverage options and costs. Understanding when to enroll can save you thousands of dollars over your retirement years.

Medigap Open Enrollment Period

Your Medigap Open Enrollment Period (OEP) begins the first month you're both 65 or older and enrolled in Medicare Part B. This one-time window offers three essential advantages:

- You can enroll in any Medigap policy sold in your state

- Insurance companies cannot deny you coverage due to health problems

- You'll generally receive better prices and more choices

Unlike Medicare's Annual Enrollment Period, your Medigap OEP lasts exactly six months. Moreover, for those still working with employer coverage when turning 65, your Medigap OEP doesn't start until you actually enroll in Part B.

Medigap OEP happens only once in your lifetime.

Guaranteed issue rights explained

Guaranteed issue rights protect your ability to purchase Medigap outside your OEP without health screening in specific situations. These "Medigap protections" typically provide a 63-day window to apply and include circumstances such as:

- Losing employer-sponsored retiree coverage through no fault of your own

- Your Medicare Advantage plan withdrawing from your area

- Moving outside your Medicare Advantage plan's service area

- Disenrolling from a Medicare Advantage plan during your 12-month "trial right" period

During these periods, insurance companies must sell you certain Medigap policies at the best available rate regardless of health status.

What happens if you miss your enrollment window

Outside protected enrollment periods, you face potentially serious consequences:

- Medical underwriting becomes mandatory, with approximately 20 health questions on applications

- Insurance companies can legally deny coverage for pre-existing conditions

- Premiums may be substantially higher

- Fewer policy options may be available

If denied Medigap coverage, Medicare Advantage plans provide an alternative since they cannot reject applicants based on health status. Essentially, these plans offer guaranteed acceptance during their enrollment periods, giving you coverage options despite missed Medigap windows.

Factors That Affect Medigap Costs

Medigap premiums vary widely based on numerous factors that can dramatically impact your monthly costs. Beyond the benefits each plan offers, understanding the pricing structures and other cost determinants helps you make financially sound decisions about your supplemental coverage.

Community-rated vs issue-age vs attained-age pricing

Insurance companies determine Medigap premiums using three distinct pricing methods, each affecting how costs change as you age:

- Community-rated: Everyone pays the same premium regardless of age. Your rates may increase because of inflation or other factors but won't rise simply because you've had another birthday. Nine states currently mandate community rating: Arkansas, Connecticut, Idaho, Maine, Massachusetts, Minnesota, New York, Vermont, and Washington.

- Issue-age-rated: Premiums are based on your age when you first purchase the policy. The younger you buy, the lower your lifelong rate. Presently, four states (Arizona, Florida, Georgia, and Missouri) permit issue-age rating but prohibit attained-age rating. Your premium won't increase due to age but may rise from inflation and healthcare costs.

- Attained-age-rated: Premiums are based on your current age and increase as you get older. Although these policies may seem most affordable initially, they typically become the most expensive over your lifetime.

How location and discounts impact premiums

Geographic location significantly influences costs. In 2023, the average monthly Medigap premium was $217, ranging from $191 in Alaska to $267 in New York. For Plan G specifically, average monthly premiums ranged from $140 in Washington D.C. to $236 in New York.

Various discounts can reduce your premiums considerably:

- Household discounts of 5-15% when multiple people in a household enroll

- Autopay discounts typically around $2-$3 monthly

- Non-smoker rates which may lower premiums substantially

Tips for getting the best price

To secure optimal Medigap pricing:

- First, compare identical plans across multiple carriers—benefits remain the same but price differences can be substantial.

- Secondly, consider Plan G or N as alternatives to pricier options.

- Thirdly, evaluate high-deductible versions of Plans F and G, which offer lower premiums with higher out-of-pocket costs.

Furthermore, shop your plan annually when rate increases occur. Many states have special provisions allowing easier switching between plans or carriers. Most importantly, remember you can change Medigap plans any time of year, unlike Medicare Advantage or Part D plans which have specific enrollment periods.

Conclusion

Navigating the complex world of Medicare Supplement Insurance requires careful consideration of several crucial factors. Throughout this guide, we've explored how Medigap plans serve as essential financial safeguards against potentially devastating out-of-pocket costs that Original Medicare doesn't cover.

The standardized nature of these plans certainly simplifies comparison shopping, allowing you to focus primarily on premium differences rather than benefit variations. Plans G and N have emerged as particularly popular options due to their comprehensive coverage and relative affordability compared to other plans.

Your enrollment timing matters tremendously. Missing your six-month Medigap Open Enrollment Period could result in higher premiums or even coverage denials based on pre-existing conditions. Therefore, marking this critical window on your calendar and taking action during this time frame offers the best protection for your healthcare future.

Price structures also play a significant role in long-term affordability. Attained-age policies might seem attractive initially but often become more expensive over time. Conversely, community-rated or issue-age plans may provide better value throughout your retirement years.

Most importantly, remember that Medigap shopping doesn't end with your initial purchase. Annual reviews of your coverage needs and available options can potentially save thousands of dollars over your lifetime. The healthcare landscape changes continuously, making regular reassessment a prudent financial strategy.

Armed with this knowledge about Medigap plans, you now possess the tools needed to make informed decisions about your supplemental Medicare coverage. Your healthcare security during retirement depends largely on these choices—take the time to evaluate your options thoroughly before committing to any specific plan.

Plan G is currently the most popular Medigap policy, chosen by about 39% of all policyholders. It offers comprehensive coverage and is often considered a good balance of benefits and cost.

Medigap supplements Original Medicare, while Medicare Advantage replaces it. Medigap allows you to see any Medicare-accepting provider nationwide, whereas Medicare Advantage typically restricts you to a network. Medigap doesn't include drug coverage, requiring a separate Part D plan if needed.

The best time to enroll is during your Medigap Open Enrollment Period, which lasts for six months starting when you're 65 or older and enrolled in Medicare Part B. During this period, you can't be denied coverage or charged more due to health conditions.

Medigap plans use three pricing methods: community-rated (same for everyone), issue-age-rated (based on age when purchased), and attained-age-rated (increases with age). Understanding these can help you choose a plan that remains affordable over time.

Yes, you can change Medigap plans at any time of year. However, outside of certain guaranteed issue situations, you may be subject to medical underwriting and could be denied coverage or charged higher premiums based on your health status.