Medicare 101

How to Choose Medicare Part D: A Simple Guide to Save Money in 2024

Did you know that in 2024, Medicare Part D premiums can range from as low as $3.30 to as high as $201.10 per month?

Understanding Medicare Part D

Medicare Part D: A Comprehensive Guide

Medicare Part D serves as the prescription medication component of the Medicare program, providing a vital service for millions of seniors and disabled individuals nationwide. When considering your Medicare options, understanding Part D thoroughly can save you significant money on medications while ensuring you have the coverage you need.

What is Medicare Part D?

Medicare Part D helps cover the cost of prescription drugs, including many recommended vaccines that aren't typically covered under other parts of Medicare. Unlike Original Medicare (Parts A and B), Part D is optional and offered exclusively through private insurance companies approved by Medicare.

These private plans must follow rules set by Medicare while providing at least a standard level of coverage. Despite being optional, enrolling in Part D when first eligible is worth serious consideration since delaying enrollment could result in a late enrollment penalty.

Currently, approximately 76% of all Medicare beneficiaries are enrolled in Medicare Part D plans. This strong enrollment rate demonstrates the essential role Part D plays in comprehensive healthcare coverage for seniors — 53 million of the 67 million Medicare beneficiaries.

How it differs from Part A, B, and C

Understanding how Part D fits within the broader Medicare structure helps clarify your coverage options:

- Part A (Hospital Insurance) and Part B (Medical Insurance) together make up Original Medicare, covering hospital stays and medical services respectively.

- Part C (Medicare Advantage) provides an alternative way to get Medicare benefits through private insurance companies.

- Part D focuses exclusively on prescription drug coverage, filling a critical gap in Original Medicare.

Notably, whereas Parts A and B are administered directly by the federal government, Part D operates entirely through private insurance companies. Furthermore, Part D stands apart because it's the only part of Medicare that's completely optional, although going without prescription coverage can lead to significant out-of-pocket costs.

Standalone PDP vs. MA-PD plans

You can get Medicare Part D coverage in two primary ways:

- Standalone Prescription Drug Plans (PDPs) - These plans add drug coverage to Original Medicare. When you choose this option, you maintain your Original Medicare coverage while adding a separate prescription drug plan. Approximately 22.2 million people use standalone PDPs (44% of Part D enrollees).

- Medicare Advantage Prescription Drug plans (MA-PDs) - These integrated plans combine hospital, medical, and prescription drug coverage in one package. MA-PDs have seen substantial growth, now covering 56% of all Medicare Part D enrollees (28.3 million people). Between 2019 and 2023 alone, MA-PD enrollment increased by 47% (9 million more enrollees).

Each approach offers distinct advantages. Standalone PDPs provide flexibility to keep your Original Medicare benefits while adding prescription coverage. Alternatively, MA-PDs integrate all benefits into one plan, often with lower premiums and deductibles than standalone PDPs. Nevertheless, MA-PDs typically come with network restrictions and utilization management requirements not present in Original Medicare.

When comparing options, remember that you cannot simultaneously enroll in both types of plans. Consequently, evaluating your specific medication needs, preferred pharmacies, and overall healthcare situation becomes essential before making this important decision.

When and How to Enroll

Enrolling in Medicare Part D at the right time is crucial for avoiding coverage gaps and unnecessary penalties. Understanding the specific enrollment windows can save you money and ensure continuous prescription drug coverage throughout your retirement years.

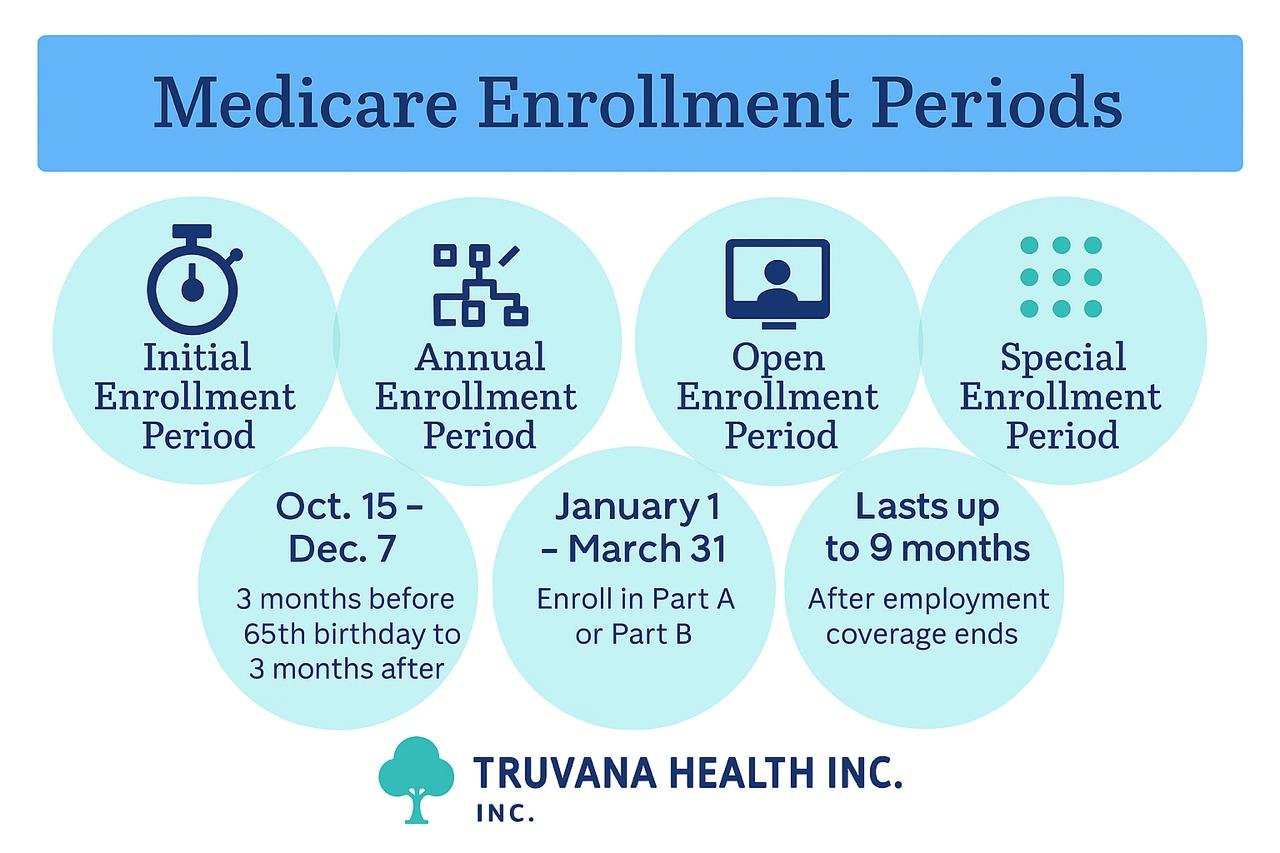

Initial Enrollment Period

—beginning three months before your 65th birthday month, including your birthday month, and extending three months after. For those eligible due to disability, this period starts 21 months after receiving Social Security or Railroad Retirement Board benefits and continues through the 28th month. Your Initial Enrollment Period (IEP) spans seven months.

When you enroll affects when your coverage begins:

- If you join before your 65th birthday month, coverage starts the first day of your birthday month

- If you enroll during your birthday month or the three months after, coverage begins the first day of the month following your enrollment

To qualify for Part D, you must have either Medicare Part A or Part B and live in the service area of the plan you wish to join. Most importantly, signing up during this initial window helps you avoid long-term financial penalties.

Annual Enrollment Period

Each year from October 15 through December 7, Medicare offers an Annual Enrollment Period (also called Open Enrollment). Throughout this timeframe, you can:

- Join a new Part D plan

- Switch between existing plans

- Drop your current coverage

Any changes you make during this period take effect on January 1 of the following year. This annual opportunity allows you to reassess your medication needs and potentially find a more suitable or affordable plan as your prescription requirements change.

Special Enrollment Periods

Special Enrollment Periods (SEPs) provide flexibility when certain life circumstances occur. These exceptions let you make coverage changes outside standard enrollment windows.

You may qualify for an SEP if you:

- Move outside your plan's service area

- Lose creditable prescription drug coverage (like employer coverage)

- Enter or leave a nursing home or long-term care facility

- Qualify for Extra Help or Medicaid

- Experience an exceptional circumstance like a natural disaster

Most SEPs last two months after the qualifying event, though timeframes vary based on your specific situation. For example, if you lose creditable coverage, your SEP begins either when you lose coverage or receive notification, whichever comes later.

Avoiding the late enrollment penalty

Failing to enroll in Part D when first eligible can result in a permanent late enrollment penalty—unless you maintained "creditable" prescription drug coverage (coverage at least as good as Medicare's standard).

The penalty equals 1% of the "national base beneficiary premium" (USD 36.78 in 2025) multiplied by each full month you went without coverage. For instance, if you delayed enrollment for 14 months without creditable coverage, you'd pay an additional 14% (approximately USD 5.20 monthly in 2025).

This penalty isn't a one-time fee—it continues for as long as you have Medicare drug coverage. Fortunately, you can avoid these penalties by:

- Enrolling during your Initial Enrollment Period

- Maintaining creditable prescription coverage (through employers, VA, TRICARE, etc.)

- Qualifying for Extra Help, which eliminates the penalty

Remember that going just 63 days without coverage after your initial enrollment opportunity ends can trigger the penalty. Thus, planning ahead for your Medicare prescription drug coverage is essential for long-term financial security.

Breaking Down the Costs

Understanding the actual costs of Medicare Part D can be challenging with its various components. I'll break down what you can expect to pay in 2025 to help you make an informed decision.

Monthly premiums and IRMAA

The average premium for Medicare Part D plans will be approximately $46.50 per month in 2025, though actual costs vary widely between plans. The base beneficiary premium is $36.78, but your specific premium depends on the plan you choose.

Moreover, if your income exceeds certain thresholds, you'll pay an Income-Related Monthly Adjustment Amount (IRMAA) in addition to your regular premium. For individuals earning above $106,000 or couples filing jointly earning above $212,000, the surcharge ranges from $13.70 to $85.80 monthly. This surcharge is based on your tax return from two years prior (2023 income for 2025 premiums).

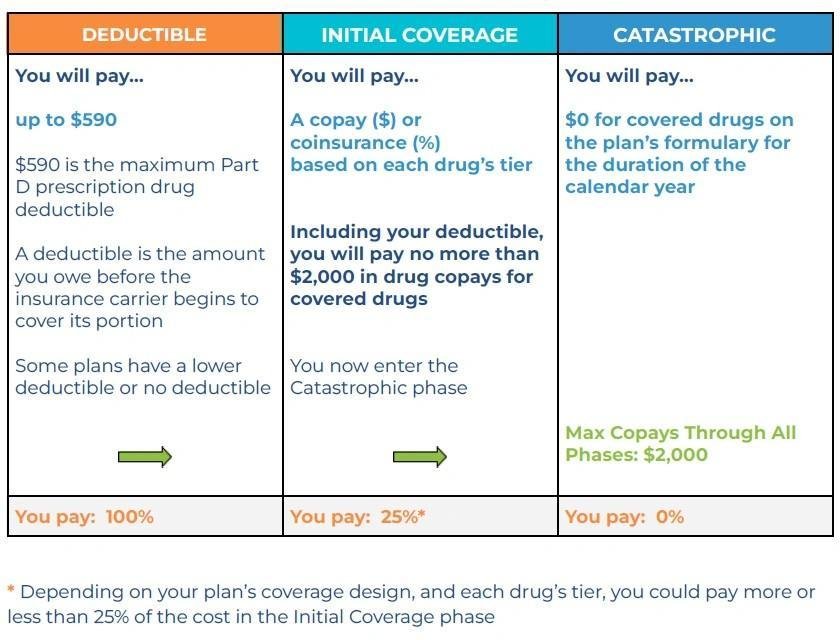

2025 Medicare deductible and copays

In 2025, the standard Medicare Part D deductible is $590, although some plans offer lower or even zero-dollar deductibles, typically with higher premiums. After meeting your deductible, you'll generally pay either:

- Copayments: Fixed amounts for each prescription

- Coinsurance: A percentage of the drug cost

These costs vary depending on your plan's tier system, with lower-cost generics typically in lower tiers.

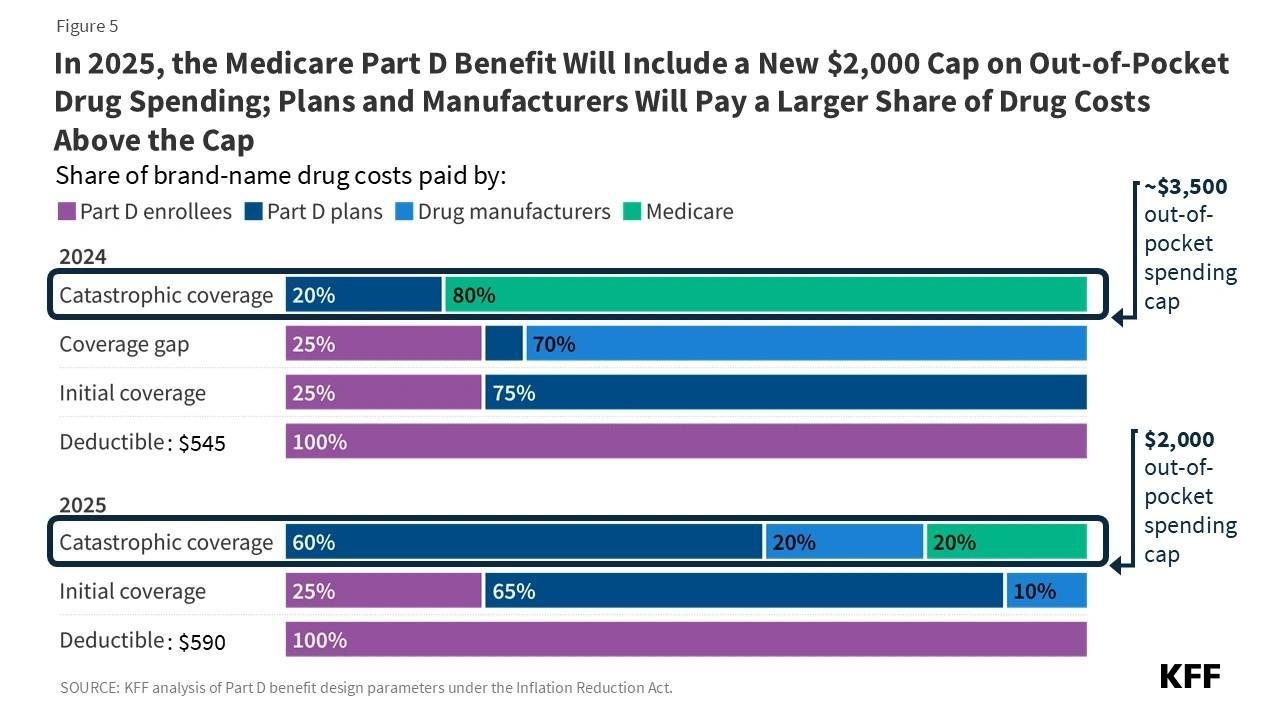

Coverage stages: deductible, initial, gap, catastrophic

Medicare Part D has undergone significant changes for 2025, now featuring three phases instead of four:

- Deductible stage: You pay 100% of costs until reaching your plan's deductible (maximum $590)

- Initial coverage stage: You pay 25% of drug costs, with the plan paying 65% and manufacturers covering 10% for applicable drugs

- Catastrophic coverage stage: As of 2025, the annual out-of-pocket spending cap is $2,000, but catastrophic coverage begins once your total drug costs—including manufacturer discounts and plan payments—exceed a specific threshold, not simply $2,000 OOP

Importantly, the coverage gap ("donut hole") has been eliminated as of January 1, 2025.

How the Medicare Prescription Payment Plan works

Starting in 2025, the Medicare Prescription Payment Plan offers a way to spread your out-of-pocket prescription costs throughout the year. This optional program doesn't reduce your total costs but helps manage cash flow.

Upon enrollment, instead of paying at the pharmacy, your plan pays first and then bills you monthly. Your monthly payment is calculated by dividing your accumulated costs by the remaining months in the year. No interest is charged, even for late payments.

This option is particularly valuable if you expect high drug costs early in the year or anticipate reaching the $2,000 out-of-pocket maximum.

Comparing and Choosing the Right Plan

Selecting the ideal Medicare Part D plan requires careful comparison of multiple factors beyond just the premium price. Finding coverage that matches your specific medication needs can save you hundreds or even thousands of dollars annually.

Using the Medicare Part D Plan Finder

The Medicare Plan Finder tool at Medicare.gov serves as your best resource for comparing prescription drug plans. This official tool allows you to enter your specific medications and preferred pharmacies to calculate personalized cost estimates. Importantly, the tool displays total yearly costs for each plan—combining premiums, deductibles, and medication copays—rather than just monthly premiums. Creating a MyMedicare account beforehand enables you to save your drug list and search criteria for future comparisons.

Understanding drug tiers and formularies

Every Part D plan organizes medications into "tiers" that determine your out-of-pocket costs. Most plans use a structure where lower tiers cost less:

- Tier 1: Most generic drugs (lowest copay)

- Tier 2: Preferred brand-name drugs (medium copay)

- Tier 3: Non-preferred brand-name drugs (higher copay)

- Specialty tier: Very high-cost drugs (highest copay/coinsurance)

The plan's "formulary" (covered drug list) dictates which specific medications are covered and in which tier they're placed. Formularies change frequently, so verify your medications remain covered each year.

Preferred vs. standard pharmacies

Within a plan's network of covered pharmacies, most plans now designate certain pharmacies as "preferred"—where your costs will be significantly lower. According to AARP research, using preferred pharmacies can save between $2 and $15 per prescription on generic drugs. Currently, 97% of Medicare Part D plans utilize preferred pharmacy networks, up from just 13% in 2011.

How to compare Cigna Part D plans and others

When evaluating Cigna or other Part D plans, focus on these key factors:

- Confirm all your medications appear on the plan's formulary

- Verify your preferred pharmacy is in-network (ideally as "preferred")

- Compare total annual costs rather than just monthly premiums

- Consider mail-order options for additional savings

Cigna's website allows entering your medications and pharmacy information to estimate costs across different plan options. Remember that plan benefits and costs change yearly, so reassess your coverage during each annual enrollment period.

Getting Help and Extra Support

Beyond selecting the right plan, several programs exist specifically to help reduce Medicare Part D costs for those with limited income and resources. These support systems can substantially lower your out-of-pocket expenses.

What is Extra Help and who qualifies

Extra Help (also called Low-Income Subsidy or LIS) is a Medicare program that assists with Part D costs, providing support worth approximately $5,900 annually per person. This program covers premiums, deductibles, and significantly reduces medication copayments.

You automatically qualify for Extra Help if you receive:

- Full Medicaid coverage

- Help from Medicare Savings Programs

- Supplemental Security Income (SSI) payments

Others may qualify by applying through Social Security if their 2025 income falls below $23,475 for individuals or $31,725 for married couples, with resources under $17,600 (individual) or $35,130 (couples). Yet even if your income exceeds these limits, you might still qualify since certain income and resources aren't counted.

With Extra Help, your 2025 costs decrease substantially: $0 plan premium, $0 deductible, and copayments of just $4.90 for generics and $12.15 for brand-name drugs. Once total drug costs reach $2,000, you'll pay nothing for covered medications.

State Pharmacy Assistance Programs (SPAP)

First established by state governments and now receiving federal support, State Pharmaceutical Assistance Programs offer additional help with prescription costs. These programs vary widely by state, with some providing wraparound coverage for Medicare Part D—essentially filling gaps where Part D doesn't cover expenses.

SPAPs coordinate with Part D plans and may help pay for premiums, deductibles, and copayments. Notably, qualified SPAPs provide Special Enrollment Periods allowing you to make changes to your Part D coverage outside standard enrollment windows.

Medicare and You 2024: where to find help

The "Medicare & You" handbook represents your official guide to Medicare programs. Mailed annually in late September, this resource contains essential information about Medicare benefits, costs, rights, and available health and drug plans.

For faster access, you can opt for the electronic version with the most current Medicare information. This handbook serves as your comprehensive reference for Medicare questions, including details about Extra Help and other assistance programs.

Additionally, the Medicare Plan Finder tool at Medicare.gov helps identify SPAPs you might qualify for in your state. Through these resources, you'll discover valuable options to reduce prescription drug expenses whenever possible.

Conclusion

Choosing the right Medicare Part D plan can significantly impact your financial well-being during retirement. Throughout this guide, we've explored how premiums can vary dramatically from $3.30 to over $200 monthly, making your selection process crucial for your budget. Additionally, we've seen how the elimination of the "donut hole" and the improved catastrophic coverage threshold of $8,000 bring substantial relief to beneficiaries in 2024.

Timing your enrollment correctly stands as perhaps the most important factor in avoiding costly penalties. The 1% monthly penalty adds up quickly and lasts for your entire time with Medicare coverage. Therefore, understanding your Initial Enrollment Period, Annual Enrollment Period, and potential Special Enrollment Periods becomes essential knowledge.

Most importantly, remember that the lowest premium doesn't always equal the lowest overall cost. Your specific medications, preferred pharmacies, and total out-of-pocket expenses must factor into your decision-making process. The Medicare Plan Finder tool provides personalized cost estimates that can save you thousands each year when used effectively.

For those with limited income, programs like Extra Help and State Pharmacy Assistance Programs offer substantial financial relief worth exploring. These programs can reduce or eliminate premiums, deductibles, and copayments for qualified individuals.

Choosing Medicare Part D coverage certainly requires careful consideration, but the potential savings make this effort worthwhile. Reassess your coverage annually during open enrollment since plans, formularies, and your medication needs change over time. This simple yet essential practice ensures you maintain optimal coverage while keeping your prescription costs as low as possible year after year.

Compare available plans in your area using the Medicare Plan Finder tool. Enter your specific medications and preferred pharmacies to calculate personalized cost estimates. Look for a plan with the lowest overall cost, including premiums, deductibles, and copayments. Ensure your medications are covered and check for any restrictions on the plan's formulary.

In 2024, the average estimated monthly premium for Medicare Part D is $46.50. The maximum annual deductible is set at $590 for 2025. However, actual costs can vary significantly between plans, so it's essential to compare total yearly expenses rather than just monthly premiums.

Enroll during your Initial Enrollment Period (IEP) to avoid late enrollment penalties. This 7-month period begins 3 months before your 65th birthday month, includes your birthday month, and extends 3 months after. Delaying enrollment without creditable coverage can result in a permanent penalty of 1% of the national base beneficiary premium for each month you delay.

Yes, you can change your plan during the Annual Enrollment Period from October 15 to December 7 each year. Changes take effect on January 1. Additionally, you may qualify for Special Enrollment Periods under certain circumstances, such as moving out of your plan's service area or losing other creditable coverage.

Yes, the Extra Help program (also called Low-Income Subsidy) assists with Part D costs for those with limited income and resources. It can cover premiums, deductibles, and reduce copayments significantly. State Pharmacy Assistance Programs (SPAPs) also offer additional help in some states, potentially covering gaps in Part D coverage.