Medicare 101

How to Choose Medicare Part C: A Simple Guide to Save Money in 2024

Did you know that nearly 34 million Americans enrolled in Medicare Advantage (Part C) plans in 2024? That’s nearly 54% of all Medicare beneficiaries, making it an increasingly popular choice.

Additionally, these plans provide valuable financial protection by capping out-of-pocket costs once you reach a certain limit. This feature can make a significant difference in your healthcare budget, especially during years with unexpected medical needs. While Medicare Advantage plans are offered by private insurance companies—leading to variations in costs, coverage, deductibles, and copays—they're required by law to provide at least the same coverage as Original Medicare Parts A and B. However, finding the right plan requires understanding how these options align with your specific healthcare needs and financial situation. In this guide, we'll walk you through a simple process to choose the perfect Medicare Part C plan for 2024 that saves you money while providing the coverage you need.

Start with Your Health and Budget Needs

Choosing the right Medicare Part C plan starts with understanding your personal healthcare needs and financial situation. Before comparing plans, take these essential steps to ensure you find coverage that works for you.

List your current doctors and medications

Begin by creating a detailed list of all healthcare providers you see regularly. When considering Medicare Advantage plans, check if your doctors participate in the plan's network. For HMO plans particularly, staying with in-network providers is crucial—otherwise, you might face significantly higher costs or no coverage at all.

Next, compile a comprehensive list of your prescription medications. Review potential plans to ensure your medications are covered in their formulary (list of covered drugs). Remember that medication requirements may include prior authorization or step therapy. This preparation helps avoid unexpected costs later.

Estimate your annual healthcare usage

Understanding your typical healthcare utilization patterns will help you select the most cost-effective plan. According to research, the average Medicare beneficiary has approximately:

- 0.23 inpatient hospital stays annually

- 3.4 outpatient hospital visits

- 0.6 emergency department visits

- 21.1 professional visits (physician and other practitioners)

If your usage differs significantly from these averages, consider how that might affect which Medicare Part C plan offers the best value for your needs.

Set a monthly budget for premiums and copays

Medicare Advantage plans vary widely in costs. Some have $0 premiums, while others may exceed $200 monthly. Beyond premiums, budget for:

- Deductibles: The amount you pay before coverage begins

- Copayments/coinsurance: Your portion of costs for services (typically 20% for Part B drugs)

- Out-of-pocket maximum: For 2025, this cap is $9,350, though many plans set lower limits

For perspective, the average monthly out-of-pocket cost in 2019 was approximately $440 for Medicare Advantage enrollees, compared to $579 for traditional Medicare—a significant difference that might influence your decision.

Remember that you must continue paying your Medicare Part B premium regardless of which Medicare Advantage plan you choose.

Understand How Medicare Advantage Plans Work

Medicare Advantage has become a popular choice for millions of Americans looking for comprehensive coverage. In 2024, approximately 54% of Medicare beneficiaries—nearly 33 million people—were enrolled in a Medicare Advantage plan.

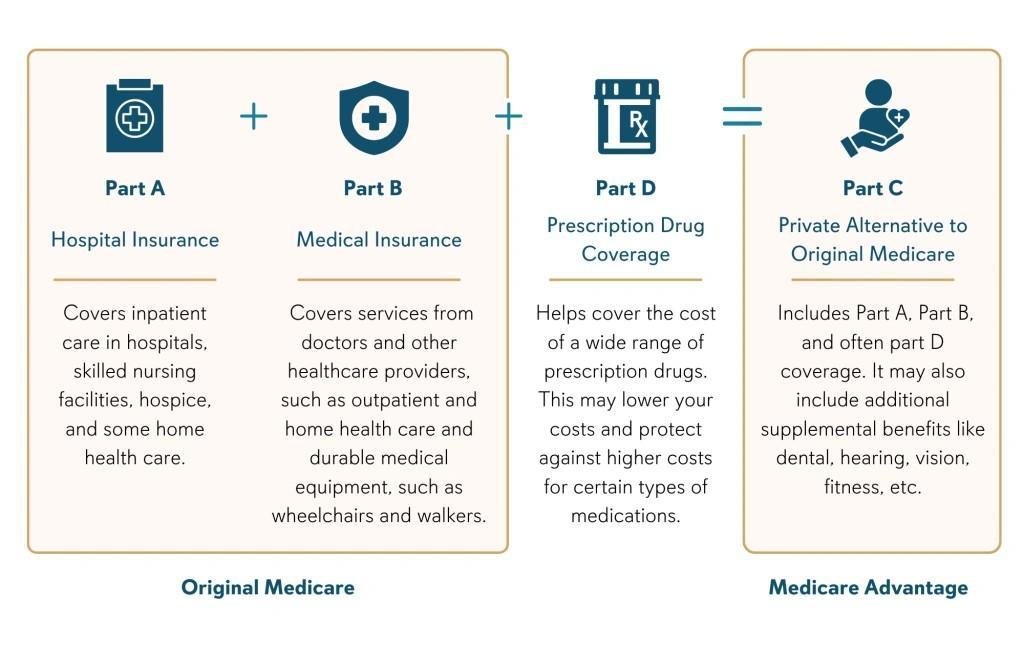

What is Medicare Part C?

Medicare Part C, commonly known as Medicare Advantage, represents an alternative to Original Medicare offered by private insurance companies. These plans bundle Medicare Parts A (hospital coverage) and B (medical coverage). Furthermore, nearly 9 in 10 Medicare Advantage plans include prescription drug coverage (Part D). Many plans also provide extra benefits not available through Original Medicare, such as dental care, vision services, hearing aids, and fitness memberships.

How does Medicare Advantage work?

With Medicare Advantage, private insurance companies contract with Medicare to provide your benefits. The government pays these companies a fixed monthly amount for your care. Unlike Original Medicare, Medicare Advantage plans feature important cost protections with out-of-pocket maximums. For 2024, the maximum out-of-pocket limit for in-network services is $8,850.

Medicare Advantage costs vary but may include:

- The Part B premium (mandatory)

- A plan premium (often low or $0)

- Copayments and coinsurance for covered services

- A plan deductible (not all plans have one)

Types of Medicare Advantage plans (HMO, PPO, etc.)

Several Medicare Advantage plan types exist, each with distinct rules:

- HMO (Health Maintenance Organization): Members typically must use network providers, select a primary care physician, and obtain referrals for specialists. These plans generally offer lower out-of-pocket costs.

- PPO (Preferred Provider Organization): Offers more flexibility to see out-of-network providers (at higher costs) and doesn't require referrals for specialists.

- Other types include Private Fee-for-Service (PFFS) plans, Special Needs Plans (SNPs) for people with specific conditions, and Medicare Savings Account (MSA) plans.

The average enrollee has 43 Medicare Advantage plans to choose from, making it essential to understand these differences when selecting coverage that matches your healthcare needs.

Compare Medicare Part C Plans Carefully

When selecting the ideal Medicare Part C plan, thorough comparison is essential for finding coverage that balances cost and benefits. Let's examine what these plans offer and how to evaluate them effectively.

What does Medicare Part C cover?

All Medicare Advantage plans must cover the same medically necessary services that Original Medicare provides. This includes inpatient hospital care, outpatient services, preventive care, and medical equipment. Moreover, most Medicare Advantage plans include prescription drug coverage (Part D).

One notable difference among plan types affects how you access care. HMO plans typically require you to use network providers, while PPO plans allow out-of-network care at higher costs. MSA plans generally don't have network restrictions, allowing you to visit any Medicare-approved provider.

Look at plan star ratings and reviews

Medicare uses a comprehensive Star Rating System to measure plan performance, with ratings ranging from one to five stars (five being excellent). These ratings evaluate plans across multiple categories:

- Staying healthy (screenings, tests, vaccines)

- Managing chronic conditions

- Plan responsiveness and care

- Member complaints and problems getting services

- Health plan customer service

Interestingly, non-profit plans more frequently earn higher ratings than for-profit plans—56% of non-profit Medicare Advantage plans received 4+ stars compared to 36% of for-profit plans. Approximately 42% of Medicare Advantage prescription drug plans earned 4 stars or higher for 2024.

Check for extra benefits like dental and vision

Unlike Original Medicare, which generally doesn't cover routine dental services, many Medicare Advantage plans offer valuable additional benefits:

- Dental coverage (preventive and sometimes comprehensive services)

- Vision care (routine exams and allowances for eyewear)

- Hearing benefits (exams and hearing aid allowances)

- Fitness memberships and wellness programs

The specific coverage varies significantly between plans. Some offer preventive dental only (cleanings, exams), while others include comprehensive services like fillings, extractions, and dentures.

To compare plans effectively, use the Medicare Plan Finder tool at medicare.gov, where you can enter your ZIP code to see available options with their costs, ratings, and benefits.

When and How to Enroll in a Plan

Initial Enrollment Period (IEP)

Your first opportunity to join a Medicare Advantage plan comes during your Initial Enrollment Period. This seven-month window includes three months before your 65th birthday month, your birthday month, and three months after. For instance, if you turn 65 in June, your IEP runs from March through September.

During this period, you can enroll in Original Medicare (Parts A and B) and subsequently join a Medicare Advantage plan. Remember that you must first have both Medicare Parts A and B before enrolling in Part C.

Annual Enrollment Period (AEP)

October 15 through December 7 marks the Annual Enrollment Period when anyone with Medicare can make changes for the upcoming year. Throughout this timeframe, you can switch from Original Medicare to a Medicare Advantage plan or change between Medicare Advantage plans.

Any plan changes made during AEP take effect on January 1 of the following year. The Medicare Plan Finder tool on medicare.gov helps compare options available in your area.

Special Enrollment Periods (SEPs)

Beyond standard enrollment windows, Special Enrollment Periods allow you to join or switch Medicare Advantage plans after certain life events. Among these qualifying events are:

- Moving to a new address outside your plan's service area

- Losing employer or union coverage

- Qualifying for Medicaid or Extra Help

- Being released from incarceration

The duration of SEPs varies by circumstance—typically two months following a qualifying event. For instance, after losing employer coverage, you have a two-month window to enroll in a Medicare Advantage plan.

An additional enrollment option exists exclusively for current Medicare Advantage members: the Medicare Advantage Open Enrollment Period from January 1 to March 31 each year. Throughout this period, you can switch to another Medicare Advantage plan or return to Original Medicare.

Conclusion

Before comparing plans, start by evaluating your healthcare usage patterns and monthly budget. Throughout this guide, we've outlined essential steps to help you navigate this important decision for 2024. Most importantly, understanding your personal healthcare requirements forms the foundation of making a cost-effective choice.

Medicare Advantage plans offer significant benefits compared to Original Medicare, particularly the added coverage for dental, vision, and hearing services. Additionally, the financial protection provided by out-of-pocket maximums can save you thousands during years with unexpected medical expenses.

Plan comparison deserves your focused attention. Star ratings provide valuable insights into plan quality, while examining coverage details ensures your specific needs will be met. Remember, the lowest premium option doesn't always translate to the lowest overall costs when considering deductibles, copays, and network restrictions.

Timing matters significantly when enrolling in Medicare Part C. Missed enrollment periods could lead to coverage gaps or potential penalties. Therefore, mark your calendar for the Initial Enrollment Period around your 65th birthday, the Annual Enrollment Period (October 15-December 7), or determine if you qualify for a Special Enrollment Period.

Medicare Part C continues to grow in popularity because it often provides more comprehensive coverage at competitive costs. The right plan can deliver substantial savings while ensuring access to quality healthcare. Armed with this guide, you can confidently choose a Medicare Advantage plan that delivers both quality care and long-term cost savings.

The estimated average monthly premium for Medicare Advantage plans in 2024 is around $18.50. However, costs can vary significantly depending on the insurer and level of coverage, ranging from $0 to over $200 per month.

You can enroll in Medicare Part C during your Initial Enrollment Period (around your 65th birthday), the Annual Enrollment Period (October 15 to December 7), or during Special Enrollment Periods triggered by certain life events. There's also a Medicare Advantage Open Enrollment Period from January 1 to March 31 each year for those already enrolled in a Medicare Advantage plan.

Many Medicare Advantage plans offer extra benefits not included in Original Medicare, such as dental care, vision services, hearing aids, fitness memberships, and wellness programs. The specific additional benefits vary between plans, so it's important to compare options carefully.

You can compare plans using the Medicare Plan Finder tool at medicare.gov. Look at factors such as costs (premiums, deductibles, and copays), coverage details, star ratings, and whether your preferred healthcare providers are in-network. Also, check for any additional benefits that may be important to you.

The main types of Medicare Advantage plans include Health Maintenance Organizations (HMOs), Preferred Provider Organizations (PPOs), Private Fee-for-Service (PFFS) plans, and Special Needs Plans (SNPs). Each type has different rules regarding network providers, referrals, and out-of-network coverage, so choose the one that best fits your healthcare needs and preferences.